Whoa! This is one of those small but big moments in crypto. My first impression was messy and excited. I mean, somethin’ about having all chains in my pocket felt like a Swiss Army knife for money. Initially I thought a single wallet that claims to do everything would be bloated and risky, but then I started testing transaction sims and risk assessments and my view changed, dramatically.

Seriously? Yes. The first thing that surprised me was how often a simulation catches gas spikes. Most wallets just show a fee estimate and leave you prayin’ for the best. A good multi-chain wallet doesn’t just estimate—it simulates the exact call, shows potential token slippage, and highlights approvals that are unusually broad. On one hand that feels like extra friction. On the other hand it’s the difference between a failed trade and losing funds to an exploit, which actually matters a lot.

Here’s the thing. Fast intuition says “more features equals more attack surface.” Hmm… my instinct said the same. But slow thinking—looking at threat models, the UI, the audit trail—shifted my thinking. Actually, wait—let me rephrase that: not every feature is created equal; some features reduce risk by adding visibility rather than adding attack vectors. So I began to prefer wallets that simulate transactions off-chain, present clear warnings, and keep approvals minimal rather than those that promise convenience at the expense of clarity.

Short stories first. I once tried a cross-chain swap that looked cheap until the sim revealed an extra wrapped-step with terrible slippage. I hit cancel. That simple interruption saved me maybe $300 that day. On a different occasion, a simulated approval showed a contract could drain tokens—not much, but it was a red flag. I revoked that approval immediately. These are little wins. They build trust slowly, like a local barista learning your order; they accumulate.

Okay, so check this out—when you stack multi-chain access with simulation and risk scoring, the math changes. A wallet that transparently simulates transactions reduces cognitive load. You make fewer blind decisions. You notice patterns—you learn which chains behave weird under congestion, or which bridges add hidden steps. And you begin to trust the tool because it taught you to anticipate failure modes instead of pretending they don’t exist.

What makes a good multi-chain wallet different?

Short answer: visibility and control. Medium answer: good UX with meaningful defaults and a sane permission model. Long answer: it’s a stack that handles network heterogeneity by simulating transactions against current mempool conditions, by parsing contract ABIs to detect dangerous approvals, and by using heuristics plus on-chain history to estimate exploit risk—so that you can make an informed choice before you sign anything.

My instinct still rebels at wallets that auto-approve everything. Seriously? That convenience is often socialized risk. On the other hand, a wallet that asks too many questions becomes unusable. So the trick is balance. For example, a wallet could ask for approvals only when necessary, offer one-click revocations from a transaction history, and present compact risk signals without burying you in technical dust.

I’m biased, but the tools that have both multi-chain reach and thoughtful risk assessment feel like the most practical step forward for average DeFi users. I’m not saying they’re flawless. No way. But they lower the barrier. Think of it like seat belts with airbags; you still need to drive responsibly, but the car helps.

Alright—let me be frank: not every “simulator” is honest. Some only replay successful paths and hide possible failures. Others simulate against stale data and give a false sense of security. So when you evaluate a wallet, ask: does it run the transaction with the live RPC on the target chain? Does it surface the exact calldata and token approvals? Can I see the probable range of outcomes, not just a single “estimated gas” number? If a product nails those, it earns trust.

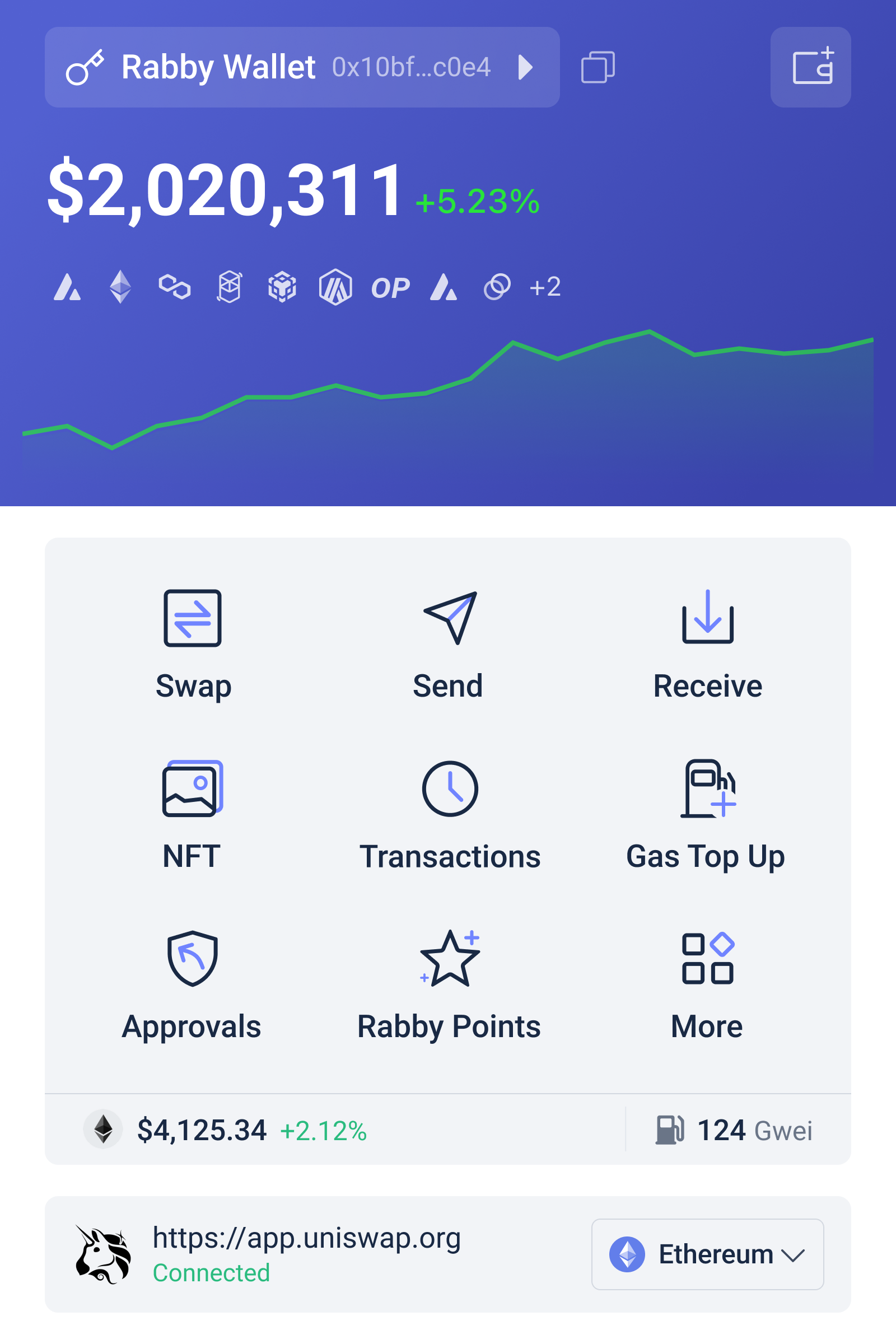

By the way, if you’re looking for a practical option that balances multi-chain convenience with transaction simulation and readable risk signals, try giving rabby wallet a look. I tested it against several real trades and found that the simulation UI nudged me toward safer choices. It’s not perfect—nothing is—but it shows the right instincts: stop-before-you-sign, explain the consequences, and let the user opt into risk knowingly.

On a technical level, the best wallets do a few things well. They parse the ABI to interpret function calls. They estimate slippage using live liquidity snapshots. They flag approvals that grant infinite allowances or that touch uncommon token pairs. They also track contract reputations using crowdsourced and historical metrics. Put those together and you move from blind signing to informed consent.

One thing bugs me: the balance between automation and human oversight. If a wallet auto-executes “gas-save” batch transactions invisibly, you might lose sight of what’s happening in your account. I prefer a model where automation is explicit, optional, and reversible. That way the user remains the actor, not the passive observer. This part of UX design is very very important.

Also, user education matters. A simulation that shows “risk: high” without context is useless. Explain why. A tooltip, a short example, even a link to a one-paragraph explanation is enough. People will read it if it’s short and specific. Long-winded handbooks? Most won’t. So keep it simple. Use examples tied to real chains people know—like pointing out how gas spiking on Ethereum mainnet during NFT drops can wreck a flash-swap, or how some bridges tack on extra wrapped transfers that increase slippage.

The psychology of warnings also matters. If you warn on every minor variance, users will ignore all warnings. But if you calibrate verbosity to severity and present the top two risks first, you get attention where it matters. On one hand you want comprehensive reporting; on the other hand you need cognitive triage. Good wallets get that triage right.

Here’s a concrete checklist I use when testing a new wallet:

1) Does it simulate transactions using live RPCs? 2) Does it show exact calldata and token approvals? 3) Can I revoke approvals easily? 4) Does it highlight probable slippage and gas volatility? 5) Are reputation signals present and reasonable? Each pass makes me more comfortable. Miss one and I get nervous again.

Initially I thought you needed a PhD in smart contracts to parse these signals, but actually, good design reduces that need. Wallets can translate “approve all” into plain English like “This contract can move your tokens without asking again.” That phrasing changes behavior. People respond to plain language. They understand “can move your tokens” immediately. On the contrary, “infinite allowance” often goes over heads, even though it’s the same issue.

Look, I’m not 100% sure about everything. There are trade-offs. A wallet that simulates more deeply requires more data, which might mean larger downloads or more calls to third-party services. That increases the surface for privacy leaks. So there’s a design tension: to simulate, you might need to reveal what you’re planning to do. Privacy-focused users may dislike that. Though actually, wait—some wallets solve this by simulating locally or using ephemeral data, which keeps privacy intact while still providing the benefit.

One more thing: community and transparency. The more a wallet opens its heuristics and logic to public scrutiny, the better. If you can inspect how risk scores are computed, or see an audit, you get a stronger signal than a closed black box. It won’t guarantee safety, but it shifts trust from intuition to evidence. And in crypto, evidence matters.

Common questions from people I talk to

Q: Can simulations be gamed or inaccurate?

A: Yes, sometimes. Simulations depend on the quality of RPC data and heuristics. They can miss front-running or mempool dynamics in volatile moments. That said, they’re still better than signing blind; use them as an extra layer of defense, not an oracle of truth.

Q: Does using a multi-chain wallet increase risk?

A: Not necessarily. A well-designed multi-chain wallet centralizes controls but doesn’t centralize vulnerabilities if it’s non-custodial. The key is how it handles private keys, permissions, and third-party integrations. Always prefer wallets with open-source components and revocation features.

Q: How often should I revoke approvals?

A: Regularly. At least after big trades or when you stop using a dApp. Tools are available that batch revocations, but be mindful of gas costs. If you don’t want to pay for frequent revokes, restrict allowances to minimal amounts to start with.